Canadian Fintech: Trade Credit 🌎

Nova Scotia... no not that one. Embedded insurance. Mortgage backed securities.

Morning!

Welcome back to Canadian Fintech, a newsletter for founders, operators & investors. Was this forwarded to you? Become one of our 7,209 subscribers by clicking below.

Do you invest in Canadian fintech? I’m putting together a list of investors to share deal flow from this newsletter. Fill out this quick form to be added to the list.

💰 Funding

Mintlist raised $2m for their online car auction platform. I see two popular models in this industry:

Holds inventory - the online platform buys, inspects, refurbishes, resells, and provides financing themselves ex. Canada Drives (until recently) and Clutch

Does not hold inventory - the platform facilitates the buying and selling, but everything else happens through a traditional car dealership ex. Mintlist, EBlock, TradeRev, and HeyAuto

NetNow a trade credit application system won $30k in prize money by sweeping the Intuit Fintech Demo Day. What is trade credit?

When b2b suppliers sell goods they often extend payment terms (ex. 30, 60, or 90 days).

But first the supplier needs to underwrite the buyer to determine if they qualify for net terms. Similar to a loan.

Today that process takes place over PDFs and emails. NetNow is digitising it.

Padder raised an angel round to help independent landlords collect rent and manage properties.

Over 70% of Canadian landlords are “mom and pop” operators.

🤝 M&A

Passiv, a portfolio rebalancing tool for passive investors acquired Wealthly, a social investing app. Why?

At first blush, this looks like a b2c play - buying a complementary consumer business for users and to compete on features with Blossom.

But really, the deal is to bolster Passiv’s b2b business, SnapTrade, a stock exchange aggregator that powers consumer facing apps like Passiv.

Wealthica offers similar wealth integration APIs.

Brane, a trust company for crypto was acquired by Wellfield, a diversified crypto company for $10m.

Though Brane had minimal market share, it was one of only a handful of regulated crypto custodians - Tetra and Balance being the larger independent providers.

SunLife, one of Canada’s largest insurers acquired Dialogue, a telemedicine startup for $277m. Why?

Digital health as an employer benefit has become an area of growth for insurers. Telus acquired Dialogue competitor LifeWorks last year for $2.3b.

👀 Looking for your next Canadian fintech gig?

If you are excited to make life better for millions of Canadian companies and teams, Float is hiring across every department.

Join one of Canada’s fastest growing fintechs and help build a platform loved by thousands of Canadian businesses. Current open roles include Engineering Lead, Senior PM, Senior Growth Marketing Manager, RevOps Manager and Customer Implementation Manager.

Float is simplifying spend so companies and teams can focus on growing their business. Our team and investors bring experience from leading software companies including Shopify, Uber, DoorDash and more.

🚀 Product

Nova Credit, a platform that connects credit bureaus around the world has launched in Canada. Why is this a big deal?

Lenders rely on credit bureau data to underwrite borrowers. This data shows a borrower’s history of receiving and paying back loans, and is used to calculate a credit worthiness score.

Newcomers to Canada don’t have any local credit history and so are “credit invisible” to lenders. If a borrower has no credit history, a lender considers them a high risk.

Canadian fintechs have been tackling this problem for years with innovations like cash flow underwriting (lending against income not credit history) and credit builder loans (a financial product that mimics the repayment of a loan to establish positive credit history with bureaus).

Nova’s first customer, Scotiabank, will now allow newcomers to pull credit reports from their local bureau and have it translated into a local format and scored.

Embedded insurance, a way to sell insurance products at point-of-sale instead of at a bank, is kinda a thing now:

Homeslice, launched a secondary market for Canadian mortgages.

Most secondary mortgage markets operate through securitization. This process allows lenders to package up parts of their loan portfolio into tranches and sell them to investors as securities. It creates liquidity for the lender and gives investors access to high yield assets.

Securitization is usually done by traditional investment banks, but online platforms like Percent.com offer similar services.

Homeslice instead is selling whole loans to investors, which can be securitized later.

🎂 Number time!

3m - the number of credit invisible Canadian adults (not enough credit data to generate a score) according to Equifax

2.7% - the amount of wealth held by the bottom 40% of wealthy Canadians according to StatsCan

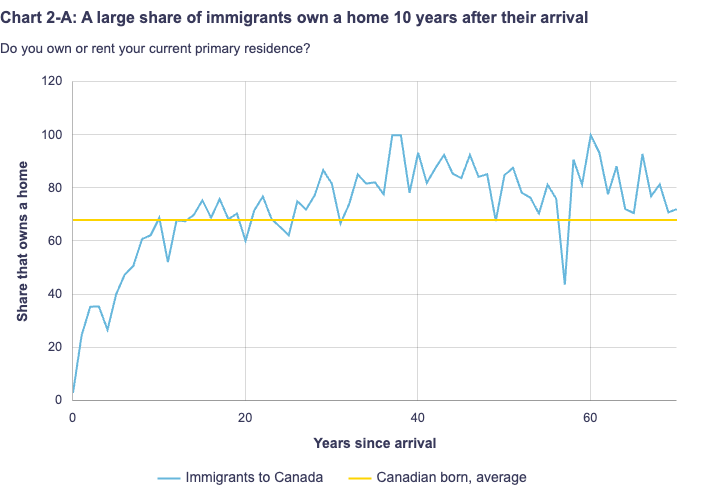

10 years - the average amount of time it takes for the homeownership rate of newcomers to equal that of the average Canadian according to the Bank of Canada (see graph below):

Do you invest in Canadian fintech? I’m putting together a list of investors to share deal flow from this newsletter. Fill out this quick form to be added to the list.

Have a great week! See ya 👋