Canadian Fintech: Who is going to buy HSBC? 🤑

Fintech for international students. Wealthsimple on a policy tear. How to rent out your spare room.

Morning!

Welcome back to Canadian Fintech, a newsletter for financial services operators. Was this forwarded to you? Become one of our 5,650 subscribers by clicking below.

💰 Funding

Sparrow raised $1m to help Canadians rent out their spare rooms. There are an estimated 12 million empty bedrooms across Canada, home to several of the world’s most expensive cities for renters. The round was led by the CMHC’s new Affordable Housing Innovation Fund, which I wrote about here.

ChainSafe raised $25m to build web3 infrastructure tools that facilitate inter blockchain operability - i.e. the ability for separate blockchain networks to send each other data.

Carbon6, a portfolio of e-com tools for Amazon sellers (inventory management, listing optimization, tracking reimbursements, etc.), raised $88m. WeCommerce is a similar Canadian company that focuses on acquiring Shopify seller tools.

Embattled lender Clearco is trying to raise $30m USD from existing investors. The fintech raised $60m at a $2b valuation only a few months ago, then laid off 125 employees, exited international markets, and cut loan origination volume. Of the $17m secured so far, $6m is coming personally from co-founders Romanow and D’Souza.

Quandri, a chat-bot for insurance brokers to automate policy origination, renewals and admin, raised $2m.

🤝 M&A

Canadian crypto lender Ledn acquired Arxnovum, a crypto investment manager. This will allow Ledn to cross-sell clients investment products.

Tenant background screening platform SingleKey acquired competitor Naborly. The merger triples SingleKey’s landlord user base.

👊 Fintechs have changed the game

Fintechs have created a movement that is redefining financial services on a fundamental level. Leveraging the power of technology, fintechs have challenged traditional products, services, and business models.

So, how are traditional financial services organizations responding?

Download RSM’s e-book to find out and access resources to help your company build a path forward.

🚀 Product

Propel, a TSX-listed consumer fintech lender, has partnered with BaaS provider Pathward (fka MetaBank) to become its primary lending partner. I wrote about how these partnerships work here.

Canadian merchants using Square will now be able to offer BNPL using AfterPay. AfterPay entered Canada in 2020 and was acquired by Square the following year.

In other BNPL news, Visa has partnered with POS Nuvei and payment-middleware Tender Retail to expand its installments product to more Canadian retailers.

There are nearly 400k international students enrolled in Canadian post-secondary education. All of those students require “proof of financial support” in order to qualify for a study permit (see screenshot from the federal website). This has created a market for fintech innovation:

Halp, a one-on-one coaching platform for international students applying to Canadian universities (degree financing, setting up bank accounts, etc.), raised $5m.

ApplyBoard, a Canadian unicorn in this market partnered with RBC to help international students open GICs (a way to satisfy the gov mandated financial support requirement).

⚖️ Policy

Wealthsimple continues its recent streak of firsts:

One of Canada’s first registered securities dealers granted membership to Payments Canada

The first fintech to sit on its 20 person Member Advisory Council

The first fintech to be approved by the Bank of Canada for direct settlement with Canada’s future money movement system, the Real-Time-Rail.

FINTRAC has published new policy interpretations that may expand Money Service Businesses (MSBs) registration requirements to businesses acting as middle-men in payment transfers or processing. MSBs are required to register with FINTRAC and report transactions over $3k.

🤑 Who is going to buy HSBC?

HSBC, Canada’s 7th largest lender is on sale for an estimated $10b - the largest sum for any bank deal. All big 6 banks have expressed interest, but RBC is the lead contender.

Why?

Since 2008 Canadian banks have been forced to stockpile cash (aka increased capital requirement) to absorb recession induced shocks.

This was compounded during Covid as OSFI restricted stock-buybacks and dividend increases - two classic ways of spending cash to increase shareholder value.

Canadian banks now sitting on huge war chests have started to spend:

TD is spending $15b US to buy i-bank Cowen & retail bank First Horizon.

While BMO is spending $17b US to buy Bank of the West.

But RBC, Canada’s largest bank by profits, has yet to spend any.

What about the others?

CIBC is already highly exposed to the Canadian market and is more likely to invest in the US than at home.

National Bank is a natural choice as it would help them expand outside of Quebec. But with a $30b CAD market cap, an acquisition that large is tough.

Scotia has the lowest capital ratio of its peers and just went through a leadership change.

And what about foreign buyers?

Citibank already has a small local presence and recently launched commercial banking.

JP Morgan is off the table as they are advising the sale.

PNB & ING has been exiting North American markets. PNB is actually on the other end of the BMO / Bank of the West transaction.

$10b is pretty expensive to become the 7th largest bank in Canada. That’s nearly 2x their book value (on the high end for even the most valuable banks).

But a local buyer may be more willing to pay a premium in the pursuit of market share and increased back office efficiencies.

Pundits scoffed at the $8b price tag on the TD / Canada Trust acquisition in 2000. But in retrospect the deal allowed TD to quickly become the country’s largest bank by assets.

The elephant in the room? Canada’s competition bureau.

Local mergers always bring more scrutiny despite Canada’s track record of allowing many to proceed cough cough.. Rogers.

With history and a strong balance sheet on its side, I think RBC is the clear winner.

🎂 Number time!

$2000 - the average Canadian monthly rent

59% - the percent of lenders now using alternative data (non-credit bureau) in their underwriting

$1.2m - the difference in net worth between homeowners born between 1955 and 1964 vs non-homeowners

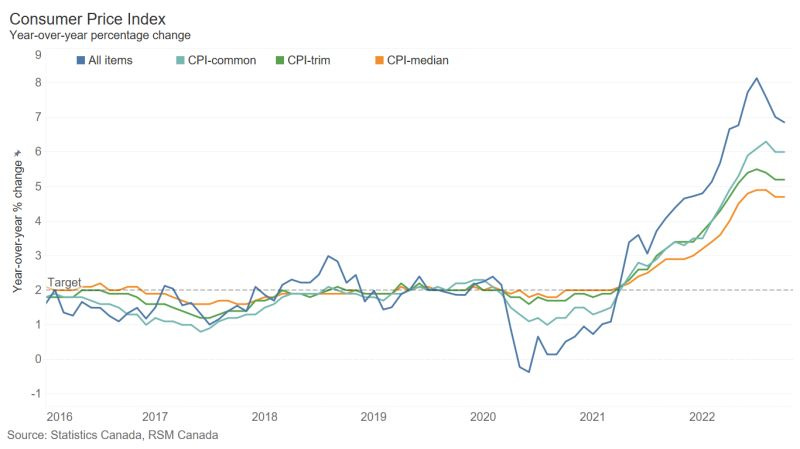

6.9% - year over year CPI inflation. Food prices have increased at the fastest pace since 1981 (11.4%).

👀 Who’s hiring?

Neo Financial, VP Product (Calgary)

Neo Financial, VP Engineering (Calgary)

RSM, Transaction Advisory Services Manager (Vancouver)

Thanks for voting in last week’s poll! The results were… divided. Out of the 52 responses I received, exactly half voted for a more frequent / shorter newsletter. I think I’ll punt this one to the new year :)

Interested in sponsoring? Reply to this email.